What are the costs of poor revenue forecasting?

TL.DR: Higher Inflation

A reader asked the expected question based of the last post, “what is wrong with monetary financing”? A good question really? The link is rather straightforward: monetary financing typically means faster money supply growth. Which, all things being equal, means higher inflation. Is this the case in Nigeria? Well yes.

Fig 1: Growth rate of money supply (M2) vs nominal GDP. Source: CBN Statistical Database1.

Of course we can remember from our Econ 101 classes. More money chasing the same goods equals inflation. Ergo, faster money supply growth with a slower economy equals higher inflation as shown in Fig 1.

I know. I know. There’s the argument about supply shocks being behind inflation but that is not really the case here. Not that supply shocks don’t matter but even if you didn’t have supply shocks you would still have higher than normal inflation because of how fast money supply has been growing.

What is the source of this money supply growth?

Fig 2: Share components of money supply. Source: CBN.

First of all, the growth in M2 has not been because of cash. In fact physical cash, the blue bars in figure 2, has become less and less relevant thanks to digitalization in finance. Yes its OK to wonder what the cash policy crisis was about. Money supply has really been driven by quasi money, or to simplify things, securities. Lots and lots of securities. And demand deposits to some extent but mostly securities.

You can think of demand deposit growth being driven by credit to the private sector but what about securities? Yup, mostly government. Mostly the federal government.

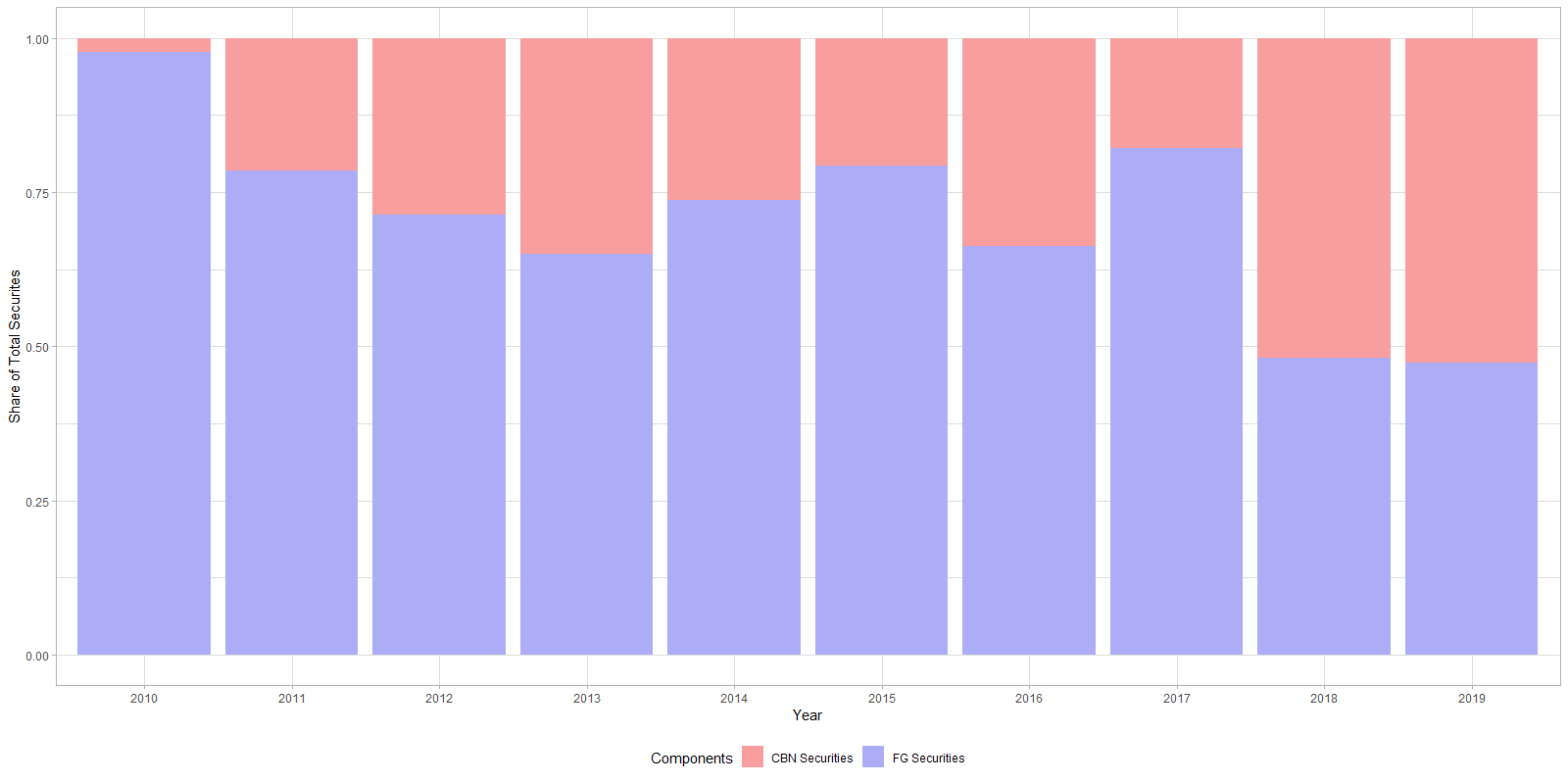

Fig 3: Share of all government and CBN securities in circulation. Source: CBN

The data stops in 2019 but I am sure you get the message. Over the last decade, as shown in Fig 3, the CBN has become increasingly responsible for the securities in circulation. Why has the CBN been issuing so much securities? To “mop up” up liquidity mostly, and maybe FX, but mostly liquidity. Why has it had so much liquidity to mop up?

Fig 4: Share of overall Net Credit - FG vs Private Sector. Source: CBN

As in clear from figure 4, the government has been responsible for an ever increasing share of net credit in the economy. If you look towards the red bars on the right, you can see the increasing expansion of government credit relative to the private sector. Who has been giving government this credit?

Fig 5: Share of claims on federal government.

Again, if you look at figure 5, which shows the components of claims on the federal government then it looks very clear. An increasing amount of credit is coming not from the private sector but directly from the CBN. And as per the last post, you know the source of that is the unapproved government deficits.

So there you have it. Unapproved deficit → expansion of credit to the FG by the CBN → expansion of money supply → inflation.

The CBN has tried to manage this expansion in money supply through other tools besides securities. Direct CRR debits have been another for instance. And again, there have been other sources of money supply expansion from the CBN besides credit to the government. Looking at you intervention funds. But in general, the major culprit is clear.

That’s enough for today.

Last word. RIP to the 41/43 items not eligible for forex list. All you did was cause distortions in the economy with no real discernible positive impact. We hope to never see your kind again.

The actual annual growth rates are the lighter color but the smooth loess function helps demonstrate the underlying trends.